Description

INV4801 ASSIGNMENT 2 2025 – FULLY ANSWERED (DUE 29 AUGUST 2025)

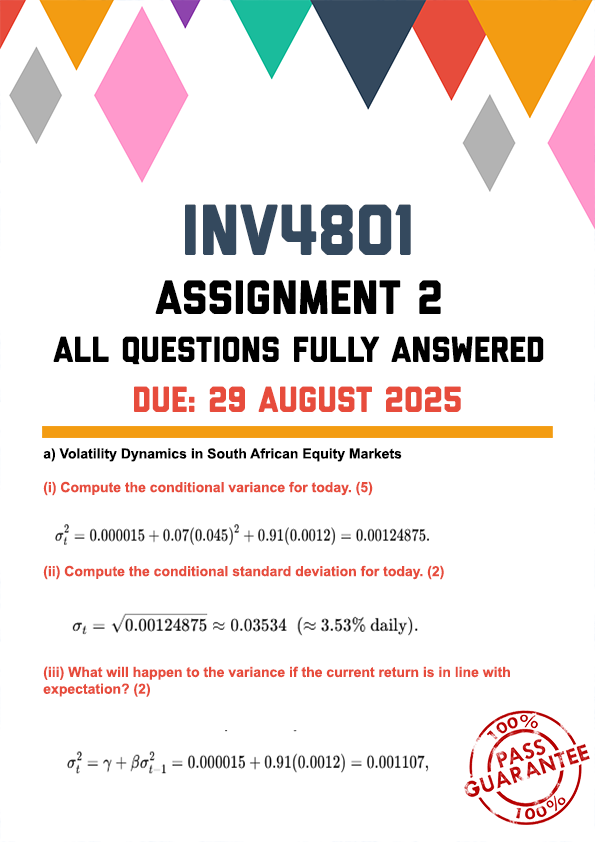

a) Volatility Dynamics in South African Equity Markets

A portfolio manager at a Johannesburg-based investment firm is tasked with managing a fund heavily exposed to the South African Top 40 Index. Following a period of heightened market uncertainty due to geopolitical tensions and fluctuating commodity prices, the firm decides to model daily equity return volatility more accurately using a Time-Varying Volatility-ARCH Models. The portfolio manager gathered the following daily information: α = 0.07, γ = 0.000015, and β = 0.91. Given these parameters, the daily standard deviation is 1%. Suppose the previous period estimated variance was 0.0012 and the current period return is 4.5% above the expected value.

(i) Compute the conditional variance for today. (5)

(ii)

Compute the conditional standard deviation for today. (2)

(iii)

What will happen to the variance if the current return is in line with expectation? (2)

Reviews

There are no reviews yet.